The fossil fuel divestment movement has been gathering pace in recent months, but is still relatively small.

A few weeks ago I attended a lecture given by Michael Liebreich, head of Bloomberg New Energy Finance, that showed just how small.

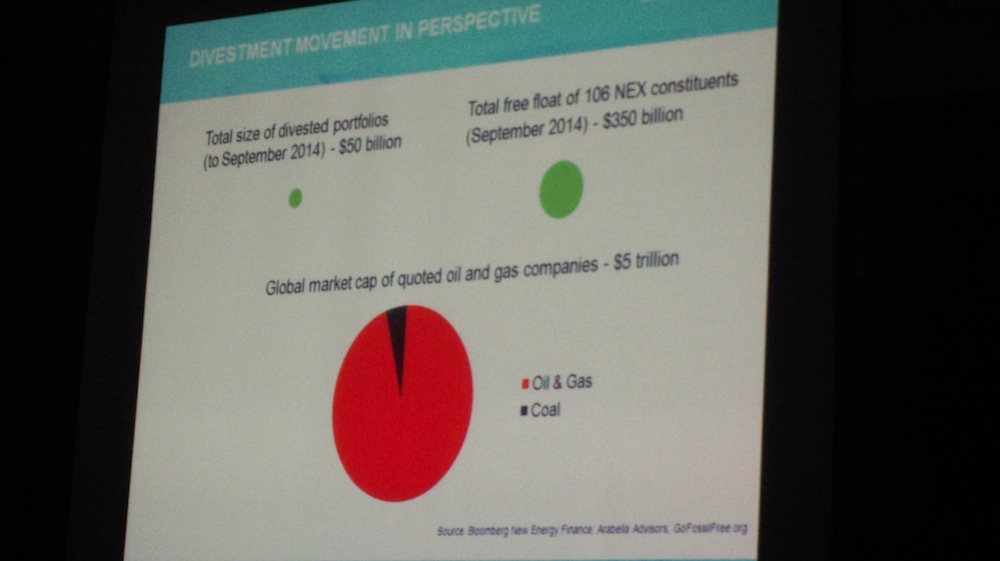

As part of his talk he briefly mentioned fossil fuel divestment, showing that it was a drop in the ocean compared with the total size of the industry. As the chart shows, the total size of all portfolios (including non-oil assets) that have divested some oil, gas or coal is $50bn, compared with a total market capitalisation of fossil fuel companies of $5trillion:

The fossil fuel industry was so large, he said, that divestment was impossible, because what other industry was large enough to put the money into instead? (And what other industry would give such good returns..?)

But the value of these firms is equal to the present value of their future free cash flows.

So what happens when the oil price falls by 50%?

If profit margins were 100% then the value of the firms would also fall by 50%.

But profit margins are less than 100%. In fact this article argues that profit margins are so slim that oil companies need to keep their tax breaks.

A quick search of the Internet brings us this chart, showing 2011 figures for “five of the largest oil companies”:

The profitability of Saudi Aramco is about 60%, of ExxonMobil and PetroChina about 10%.

If we assume these figures are indicative for all the other oil companies, and that they still apply in 2014-15, and if we assume that the current low price of oil would continue out into all future years, then this chart is shocking.

As a rough order of magnitude let’s say that the oil price has fallen 50% (from $110/bbl to $55/bbl).

According to the above chart, Saudi Aramco is still in profit, but only just (assuming profit margins were over 50%).

ExxonMobil and PetroChina are now making a loss of about 40% of the old revenue, or 80% of the new revenue. And the situation for Venezuelan PDVSA is even worse.

Assuming the low oil price continues, and based purely on these very rough indicative figures, all three companies except Saudi Aramco just went bust. And there will be knock-on impacts on (for example) the pension funds invested in them, so we will all feel the pain.

Of course ExxonMobil is “too big to fail” and all the companies can probably ride out one bad year. Bloomberg quotes one analyst as saying “An all-out price war could take up to 18 months to play out“. The question is, which firms backers have the deepest pockets.

At the end, some firms will be left standing, and world production capacity will have fallen, and prices will rise as capacity again matches world demand.

Goldman Sach’s estimate (in the same article), based on a $70 oil price, is that $1 trillion of investments in future oil projects are no longer profitable, equivalent to 8% of current global demand.

So, what will actually happen depends on how low the oil price stays, for how long. Only the big players in the game can know what they intend to do.

But as a rough order of magnitude, we can say that the drop in oil price is effectively divesting a minimum of around 8% to 20%* of the world’s oil and gas industry, without transferring that value into other industries first. Possibly more. (And possibly less.)

(* 8% of capacity, and $1tn/$5tn.)